|

|

|

|

|

Pension debt: A public policy disaster Originally posted August 1, 2016; corrected 1/6/2017

I've said in earlier stories that Lansing's unfunded liability for City retirees is $791.5 million. With 48,288 households in Lansing, $791 million comes to over $16,000 per household. With a population of 115,056, that is $6,880 for every man, woman and child.

I'm not making this up. It comes straight from the actuary reports.

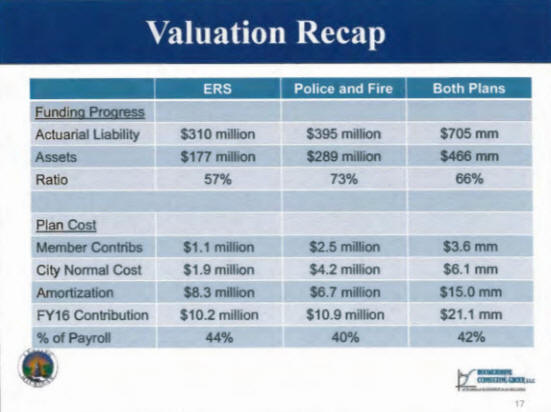

There are two parts to the debt: a) pensions and b) retiree health care benefits. Pension debt is $239 million and retiree health care debt is $552.5 million, for a total of $791.5 million. My figures are confirmed by a presentation by the City's actuary in February 2015. This page from the presentation says total actuarial liability for pensions is $705 million and total assets is $466 million. The difference is $239 million.

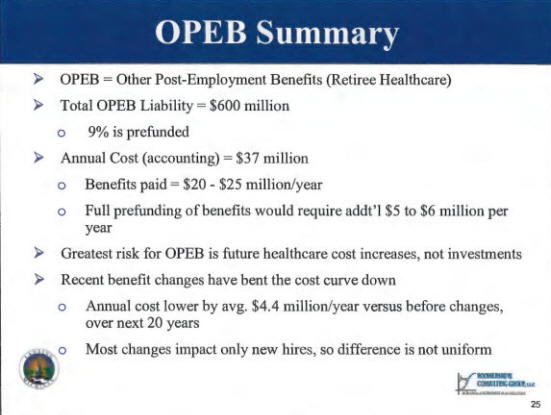

This page says total retiree health care benefit liability is $600 million and it's 9% prefunded. 91% of $600 million is $546 million. (My $552.5 figure is a little high. I'm sticking with it until I see a more recent actuary report.)

And Lansing's is not the only pension debt for Lansing residents. We are also residents of Ingham County and the state of Michigan and we are responsible for their pension debt, too:

The above doesn't include the unfunded liability for retiree health care benefits.

This is from Lansing mayor Bernero's cover letter for the 2015-2016 Executive Budget Summary:

Of that $45 million, $6 million is for pension benefits earned in the current year, $15 million is a payment on the pension funding shortfall and the rest is for retiree health insurance. The City's total budget is $196.3 million.

Lansing is one of Michigan's big five when it comes to pension debt:

East Lansing has a serious pension underfunding problem, too. This story from EastLansingInfo.org says pensions are underfunded by $71 million, and the city is waiting on an actuarial report to learn the amount by which retiree health care is underfunded.

How did we get into this mess?

In 2001, Lansing's Police & Fire Retirement System was 112.6% funded and the Employees Retirement System was 89.5% funded. Together, they were 101.9% funded. Things went down hill from there:

In the February 2015 presentation by the City's actuary, these possible causes are listed:

For the Employees Retirement System, a contributing factor was the early retirement incentive of 1992. In a collective bargaining session early that year, a very generous offer was presented to Teamsters union representatives. Teamsters who agreed to retire by January 4, 1993 would get their pension multiplier increased from 2.5% to 2.75% and they'd get an extra 5 years of service credit. That extra 5 years of service credit was not just for the pension calculation, the formula for which was years of service times FAC times the multiplier. It could also be used in determining when an employee could retire. And due to personnel rules OK'd by City Council in 1985, executive and exempt employees were tied to contracts negotiated with the Teamsters. In all, 144 employees - 12% of the City's workforce - took the offer. Here's the breakdown by age:

More on Lansing's early retirement incentive of 1992 here.

Another big contributor to the pension funding shortfall was the Great Recession of 2008, when both pension fund investments and tax revenues took a hit. Still, the City has been diligent in making the annual payments to the retirement funds recommended by the actuary - for pensions, anyway. Retiree health care is another matter. That traditionally has been a pay-as-you-go item. Only in recent years have officials realized that health care costs need to be pre-funded just like pensions:

Lansing's actuarial valuations for retiree health care exist for only the last few years (and are hard to get your hands on).

Retirement boards

For decades, pension systems have been overseen by boards with the responsibility for making sure pensions are granted in accord with city ordinances, that pension funds are invested wisely, and that the City makes contributions to the fund in the amount determined by the actuary. The board for Lansing's Employees Retirement System (ERS) consists of the mayor, a member of the City Council, the City Treasurer, the Human Resource Director, three members of the system (active employees), a retired member of the system and a city resident. The board for the Police & Fire Retirement System consists of the mayor, a member of the City Council, the City Treasurer, two members of the Police Department, two members of the Fire Department and a city resident. The boards meet monthly. Current members of each board are listed here.

Mayor Bernero seldom if ever attends retirement board meetings.

The retirement boards have no responsibility for retiree health care funding. That responsibility lies with City administration.

Why weren't city officials and retirement board members sounding the alarm when, in 2003, pension funding shortfalls began jumping by $10 million a year, peaking with a $53 million increase in 2012? It wasn't until the fall of that year that Mayor Bernero appointed the Financial Health Team to look into the situation. The Team's report in March 2013 put total unfunded pension and retiree health care liability at $550 million.

Solutions

We can increase taxes and fees. We can cut costs by cutting City services. The City's workforce has already been cut dramatically; active members of the two retirement systems went down from 1,068 in January 2010 to 652 in January 2016 (while retirees went up from 1,441 to 2,547). We can cut costs by finding efficiencies and collaborating with neighboring jurisdictions to provide services jointly. Lansing's Financial Health Team is still hard at work looking for solutions. But keep in mind that each dollar of increased taxes and fees comes out of our pockets and could cause people to move out of the city, reducing the tax base. Each dollar saved from increased efficiency could have been used to fix our streets, eradicate blight, provide services to the needy. Money raised by whatever means to pay off pension debt does nothing for us but correct the blunders of past and present city and state officials.

There are no good solutions; this is a huge public policy disaster.

Ending pensions

While there is no escape from public pension debt, we can stop it from increasing. We can stop offering pensions and retiree health care to new employees. In private industry, workforce participation in defined benefit-only plans has gone from 28% in 1979 to 2% in 2013 (source). Meanwhile, state and local government worker participation in defined benefit plans in 2013 was 78% (source).

Unions know that pensions are complicated, and that makes them a good way to conceal excess compensation. It takes an actuary to calculate the present value of retirement benefits, and that, plus salary, is the full compensation amount. In an earlier story, I calculated the value of pensions and retiree health care for Lansing's police and firefighters as over 50% of salary and argued that spending more on salaries and less on post-employment benefits would make it easier to attract new recruits.

New employees would have to be paid extra to make up for not being eligible for post-employment benefits. Increasing salaries by the present value of the those benefits, however, is likely to make them higher than necessary to attract qualified employees - higher than the market rate. To make new employee compensation equitable with employees who will be eligible for a pension, we'd have to reduce the salaries of the latter.

Not offering pensions also eliminates administrative costs. Below are the combined costs from the 2016 projected budgets of Lansing's two retirement system boards (P&F and ERS):

Correction: The above figures are way too high. They were from projected budgets for the two systems. Actual costs for 2015 were slightly over $2 million. See Operating expenses on this page.

Of course, those administrative expenses will continue for another 70 years or so, until the last pension recipient is dead - unless we buy out the pensions. We don't currently have the money to do so, but we could borrow it.

Ending collective bargaining for public employees

Currently, no changes in City of Lansing employee compensation can be made without union approval. Contracts are negotiated behind closed doors by a mayor-appointed labor relations director and ratified by the City Council, whose members seem to believe that refusing to ratify could be considered failure to bargain in good faith, an unfair labor practice. I wrote a story about this in November 2012. Correction: If any Lansing City Council member really believed that failure to ratify a contract could be considered failure to bargain in good faith - and I'm not sure any did - they would be wrong. Lansing's city charter says "Collective bargaining contracts shall become effective when ratified by the City Council in accord with State law," which implies that they can vote "no," and that any contract is tentative until ratified. "It is a general rule in public employment that a collective bargaining agreement negotiated by representatives of the employer must be ratified by formal action of the governing body in order to be effective." (source)

The mission of union representatives in a collective bargaining session is to get as much as they can for their members. If they settle for compensation at the market rate, they have failed, since the employer already pays at least that in order to fill positions. We can assume, then, that where there is collective bargaining, employees are paid in excess of the market rate - the employer is overpaying for labor. In the case of Lansing and many other Michigan cities, that excess compensation is in pension and retiree health care plans. Since the source of the unfunded pension benefit burden is the collective bargaining session, it is unrealistic to think that's where the necessary changes are going to be negotiated. Collective bargaining is an obstacle to solving the problem of under-funded pensions.

Collective bargaining was forced upon local governments and public schools in 1965 with passage of the Public Employment Relations Act (PERA). Our state legislature could make it easier for municipalities to deal with overwhelming pension debt by repealing PERA and returning to elected city councils, county commissions and school boards the power to set employee compensation.

Send comments, questions, and tips to stevenrharry@gmail.com. If you'd like to be notified by email when I post a new story, let me know.

|